Nanosolar was a high-risk entrepreneurial foray into the world of energy, semiconductors, and manufacturing, which I made to make a difference on making green energy broadly affordable. I ended up mobilizing a Google quality team and $500+ million in capital from blue-chip investors for one of the industry’s most serious efforts to make a 10x difference in solar power technology.

The plan we had was ambitious and included reinventing virtually every aspect of a solar electricity cell, applying novel processes to novel substrates with novel tooling. The goal was to arrive at a highly efficient solar cell composed of cheap Aluminum foil with a thin film of a semiconductor printed on top of it (as well as 15 other low-cost ancillary layers). No other company had ever replaced semiconductor processing with simple printing. No efficient solar cell had ever been produced based on the cheapest of all conductive foils.

It took a torturous amount of perseverance, determination, and outside support to get all that innovation working. In the end, our team did manage to deliver numerous against-all-odds technological breakthroughs and translate them into two dozen completely new manufacturing processes and tooling designs and implement them all the way in two state-of-the-art fabs, which ramped over time to >90% end-to-end yield. World-record efficiencies were achieved. The world’s largest utility backed us with a binding $1B purchase contract. The smartest investors piled in. And the list goes on.

Yet it ultimately failed commercially. Like essentially every other solar tech co it turns out. (Sadly, this became an industry where no tech co truly succeeded and only businesses based on financial engineering are now seeing some success.) As usual, whoever does anything makes mistakes, and we made plenty of mistakes. But so do people in many startups that succeed greatly.

In hindsight, I would not touch a business again with any of these three attributes — they simply make it too hard to succeed as a startup: 1. Long product reliability testing required. 2. Many production steps with statistical yields. 3. No China story upfront. The solar panel business had them all. As a startup, one needs fast development cycles, and then fast access to customer dollars once a product is developed. Observing a solar field installation for a year to prove a product keeps performing is not part of that. (Btw, other industries like battery technology are not at all better on that, and thus similarly unsuited for startups in my view.)

More detailed history on Nanosolar:

With my initial entrepreneurial success in Internet software giving me the freedom to do whatever I thought is most worthwhile, in 2002, I decided that it would be meaningful if I’d be able to bring to bear a Silicon Valley type approach to making a difference on difficult technological challenges in the area of sustainable / green energy. I picked the then rather uncharted frontier of solar power. Product and factory cost were holding back solar in a major way from its obvious potential. The question was how to make a big leap of a difference on cost and capital efficiency.

Various inventors had been pursuing novel semiconductor process technologies but few did much to turn this into real products. There was a lot of pioneering science out there but little really intense, focused commercial development. We set out to change that and go after the most promising route in a commercially meaningful and intense way. It did in fact turn out to be difficult, if ultimately in unexpected ways.

Pursuing the endeavor involved basically two grand bets — whether it’s possible to achieve technological breakthrough in a completely new area using a certain style of approaching things; and whether it’s possible to finance such an effort with the hundreds of millions of dollars it requires.

The technological grand experiment — being able to master incredible innovation in green energy technology — basically worked out fine. Smart engineers put behind the right goals and equipped with good funding can truly move mountains and, with intense work, prove all sorts of nay-sayers wrong (and there’s plenty of them at any time). It is always difficult for people at the outside to fairly judge what someone is making under the hood of commercial secrecy — blog and press coverage fluctuated somewhat randomly from exuberant to fatalistic. But the benchmarking we did with CEOs of other leading manufacturers were much clearer feedback: Whenever we showed one of them what we have under the hood (and we did not mind doing that), their jaws would usually drop to the floor by the end of the tour. The European ones tended to say that our team had accomplished in 6 years what their heavily subsidized groups did not get anywhere close to achieving in 20 years. That was the crux of the matter: Huge acceleration and leaps are in fact possible in greentech with a startup style of research and development, and untapped opportunities abound left and right in science based innovations pursued with a startup mindset.

The technological grand experiment — being able to master incredible innovation in green energy technology — basically worked out fine. Smart engineers put behind the right goals and equipped with good funding can truly move mountains and, with intense work, prove all sorts of nay-sayers wrong (and there’s plenty of them at any time). It is always difficult for people at the outside to fairly judge what someone is making under the hood of commercial secrecy — blog and press coverage fluctuated somewhat randomly from exuberant to fatalistic. But the benchmarking we did with CEOs of other leading manufacturers were much clearer feedback: Whenever we showed one of them what we have under the hood (and we did not mind doing that), their jaws would usually drop to the floor by the end of the tour. The European ones tended to say that our team had accomplished in 6 years what their heavily subsidized groups did not get anywhere close to achieving in 20 years. That was the crux of the matter: Huge acceleration and leaps are in fact possible in greentech with a startup style of research and development, and untapped opportunities abound left and right in science based innovations pursued with a startup mindset.

The other grand experiment was whether it’d work to expand the realm and horizon of high-beta investors into greentech — and associated with this: 7-year development cycles, seriously international business, global manufacturing, the risk of blow-ups that kill people and necessitate large-area evacuations, and a lot of other big-boys stuff. Solar technology had been completely uninvestible in Silicon Valley and elsewhere. In 2002, no fund had ever invested in a solar company. Kleiner Perkins was contemplating greentech but not committed to it yet. Their feedback to us back then was: “What is the value proposition of solar power?” (after a pitch on printed solar versus other technologies). A Nobel laureate venture partner at a leading other firm suggested “We don’t do that in Silicon Valley — try go and speak with GE.” Planning to do manufacturing was not something anyone could remember having heard of lately. (“Last time anyone manufactured here must have been more than a decade ago.”) Venture investors had clear screening criterias which excluded anything energy, anything green, and in particular anything manufacturing. Today many investors are gone and effectively back to these criteria, possibly for good reasons. (Still overall, not the result that optimizes the common good in the best way — see also Why Facebook is killing Silicon Valley.)

Still in 2002 I felt we ought to be able to bring Silicon Valley type technological and company-building capabilities to this important industry. Given our non-China location, it was clear that our value would be in innovation and we would have to go very much for a plan of developing the ultimate solar electricity panel with maximum conceivable cost and capital efficiency. Nothing else would have been investible here (and I did try). We figured out what kind of a plan this would need to be technically–a plan that changed very little over ten years. (And once on that track, it was rather difficult to soften this towards a not-quite-as-radical-low-cost but faster-to-market approach.)

When one is targeting an entire factor of a cost reduction on a manufactured product with many components, it does not suffice to just deliver a massive innovation on one component — because improving one 15% component by infinity basically just makes that 15% difference overall. So this quickly becomes an all-out effort to develop completely new processes and designs for every component all the way, with hundreds of engineers at the company and its suppliers. We were fortunate to be in the historically unique position to do just that. (Here’ the detailed technical white paper. The really fun — technical — stuff I’m afraid I can’t discuss here. I can only say there’s been amazing innovation at every level.) With enough capital and years of persistence, the right team can keep hammering out the details and deliver some pretty incredible innovation on some very audacious goals. And that’s what we did.

I got Nanosolar going with the help of a few Internet angel-investor friends of mine, including Sunil Paul, Mark Pincus (who I had co-run a company with), Reid Hoffman (who I first met when both of us worked at PARC in the late 80s) as well as Sergey Brin and Larry Page (who I went to school with). The latter put in a marginal amount but back then they were not even liquid with their Google stock and it was a first investment for them. The quality of these initial supporters ultimately led to the fact that we became the first company to obtain funding from venture capital investors. (Benchmark Capital and USVP ended up being Nanosolar’s initial venture investor. USVP exited at a profit of a small multiple in 2005 when I shifted the company’s printable solar cell development from a highly instable and expensive organic semiconductor to the relatively a lot more established CIGS semiconductor, a move that they did not subscribe to. The other organic PV companies there were soon went out of business, so that was a bullet dodged early!) Btw, many of the early investors did actually very well with their investment — they all had a chance in 2008 to take some of their investment off the table at a 125x increase in share price, that is, if someone sold only 20% of their shares at that 125x, this still delivered a 25x overall return even if one completely discounts the remaining 80% holding. Some of the later strategic investors bought supply optionality which was important to them beyond the value of their investment. (Plus Goldman Sachs did the due diligence for them.)

Without being particularly interested in it and certainly not actively pursuing it, we received a lot of media interest. We were always amused when people thought that we had an entire team of public relations people on staff at Nanosolar. In fact we had none. We were way too frugal for that. (Investors often called us the most frugal company with the most capital they’ve ever seen.) This approach worked for many years except later when media sentiment turned on everything including the entire industry. Initially media interest centered around Internet entrepreneurs/investors attacking a completely new industry.

The New York Times, June 19, 2003

$6.5 Million Being Invested in a Venture on Solar Cells

The NY Times first reports about the formation of Nanosolar: “Nanosolar is seen as a harbinger because of the strong pedigree of the venture capital firms and the track record of its chief executive and co-founder, R. Martin Roscheisen”

USA Today, CNN, April 26, 2004

Clean-tech firms attract growing share of venture dollars

An article syndicated by the Associated Press in major publications around the world reports about Nanosolar “turning heads in Silicon Valley” with a new solar ink.

San Jose Mercury News, Aug 15th 2004

World events spark interest in solar cell energy start-ups

The lead article in the Silicon Valley’s Mercury news: “Nanosolar’s Roscheisen embodies the new interest among Silicon Valley veterans in solar.”

Fast Company, Nov 30, 2004

Green Power

“The time may finally have come for these champions of on-the-verge technologies.”; “Roscheisen funded the company’s early research himself, and with angel investment from friends such as the founders of Google, but eventually he decided to raise $6.5 million in venture capital.”

History Channel, Dec 30, 2004

Modern Marvels: Energy Technology [Video]

First public footage of Nanosolar’s prototype coater in a History Channel episode on “staving off the looming global energy crisis”.

National Geographic, Aug 2005

Powering the Future

A cover story in the National Geographic about interest in alternative forms of energy including Nanosolar.

Motley Fool, Jan 20, 2006

Is the Price of Power Getting You Down?

A first mention in the Motley Fool: “Unfortunately, ordinary folks can’t invest in it yet.”

Business Week, June 20, 2006

Green Growth Areas for Entrepreneurs

“When technology entrepreneur Martin Roscheisen was looking for the next big thing in 2001, the Internet wasn’t part of his plans. Instead, he looked to the field of solar photovoltaics (PV), specifically at work being done by a small research company named Unisun Corp. Roscheisen recruited one of Unisun’s main researchers, and sought funding in California’s Silicon Valley. The pitch: thin-film solar cells that could be produced for less, more efficiently, and on a significantly larger scale than standard solar paneling.”

Some of the coverage above implied hopeful expectations about how quickly this potential impact would materialize. In these early years, this was in part due to the writers not understanding that putting atoms on top of each other is very different than an IT product where one assembles some components; in part due to my not taking particular care of making that clear. In a sense, I was more concerned about making payroll — already twice we had gotten to within hours of bouncing checks — so enthusiastic press coverage was surely welcome if it builds some more general support for this new area.

The crux about Nanosolar was to make solar production more capital efficient in particular. It’s difficult to see a viable business or industry if it costs a dollar in capital expenditure to generate a dollar in revenue. Capital efficiency continues to be the Achilles heel of the solar industry, and Nanosolar planned to get (and did get) a factor ahead of everyone in this area.

Even though a far more capital efficient technology, our capital requirements were still stiff. It’s developing a completely new semiconductor process and tooling to produce it. So we constantly had to make sure we had sufficient capital. Nothing worse than a fabulous engineering effort that runs out of money. And fortunately we had gotten the timing just right. The energy macro was taking off. Kleiner Perkins had made a decisive public commitment, and even we did not end up working with them, their signaling is read by a lot of investors. Around 2005 I remember being at an increasing number of dinners with pension funds and other large “LP” investors asking me which venture fund I know who invest in greentech. Predictably, soon basically every VC firm on the planet had at least one partner dedicated to greentech. It was the luck of a rising tide in which Nanosolar ended up having an unfair advantage due to being early. (This also led to a lot of envy by others as well. Of course, the envious ones tend to forget that someone else prepared the road for them in the first place.)

With our early start, we were able to scoop up an immense pool of talent. Our hiring was extremely selective, focused on raw talent and curiosity and drive more than experience. We’ve always found that issues and challenges change way too fast during the course of development, that it’s best addressed by all-around smart people whose curiosity has a burning intensity capable of making things work that others wouldn’t even try. I had seen this earlier in the Internet space in the late 90s where lots of companies got started but few had typically more than two or three truly great engineers — and then Google came along and had a complete pool of truly great ones. One of the things I was most proud of at Nanosolar is that we clearly had this pool of dozens and dozens of engineers each of which of star quality. Even the consultants we had working for us (under NDA and other IP protection) included individuals such as Gronet and Basol, who later founded Solyndra and Solopower respectively. (Btw, as for other companies abusing taxpayer funds, at least I am on the public record and also here for warning of the latter to happen. I mean this was a company whose solar product had half of the semiconductor material not in line of sight with the sun.)

The quality of our effort and early lead also exhibited in the quality of the partners we were able to engage with. The world’s largest utility ended up backing us effectively with their balance sheet — they signed a $B worth of legally binding purchases — and the CEO of the largest developer of large solar power plants in the world spent personally hundreds of hours assisting us with product definition and roll-out. It was truly wonderful.

Raising capital was never as easy as some may think given the fact that we raised half a billion in development funds. For what we were trying to do, it basically required coming up with entirely new ways of raising capital. That took a lot of creativity and effort which many others failed at. It’s one thing to raise capital if there exist funds focused on your company’s industry/stage/product; it’s another thing if there don’t. We never worked with any investment bank; pretty clear they would have failed. These were pioneering forms of raising capital. Our 2006 and 2008 financings were each the largest of any private tech company on the planet in each of these years. “Up” rounds every single time even though we often did not have much to show for yet. The experiential upside of not being able to just drive up and down Menlo Park for fund raising was an assortment of memorable meetings — such as a Sunday afternoon tea in Kuwait with Mr. Oil (OPEC’s Secretary General), a lunch at the city of London’s very much most elite members’ lunch club (where my lunch partner discussed Russian capital “that desires to become legitimized” at our table which was within hearing distance of each of those of the Chairmen of Goldman Intl and Exxon); etc.

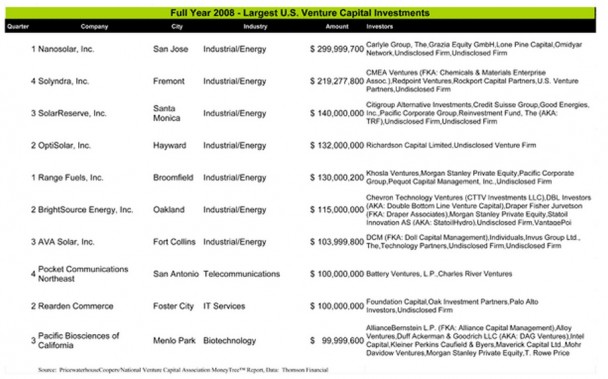

Above: Largest venture financings in 2008 is dominated by solar companies, with Nanosolar at #1.

Above: All-time (1970 thru 2009) largest venture financings as of 2009. Three greentech companies, including Nanosolar. Just two years later, this list would look completely different with ‘social media’ companies all over.

I was Nanosolar’s Chairman & Chief Executive Officer from the company’s inception in 2002 through commenced “normal production” in 2010. With our industry flagship status, I got invited to every world leader and political hob-nobbing conference on the planet; I never hesitated a second to decline them all. I was always highly suspicious of startup CEOs going to certain conferences; I would not ever invest in any such companies. Instead I myself enjoyed spending my time in the details of managing the technology development, architecting the product and process with the team. What I really enjoy most is to be able to show up at work and have really smart, really motivated engineers there, cranking on something magic.

In lockstep with a very experienced manufacturing executive, Werner Dumanski, we managed to go from the “against-all-odds” nanoscience research to manufacturing process development, production tooling development, product development including some rather challenging work on product reliability and certification.

Werner had previously run all of IBM’s $4B storage-disk operations, with 14,000 employees in his organization. It’s an example of what’s great about Silicon Valley. IBM at one point noted that one of their storage-disk factories in Germany did a far better job than its team in San Jose which had invented the very technology. Puzzled about that, they asked the leader of that group to report to work in San Jose the next Monday. That was Werner. Soon the U.S. operation was in shape: high yield and lean. And Werner ended up managing all of manufacturing at IBM. Now in Silicon Valley, he joined us at Nanosolar, initially with a staff of zero and a $1B smaller budget. Werner had all the attributes of a “level-5 leader” and I backed him fully all the way to the extent of my own ouster instead (which did not avoid his in the end though).

A unique aspect to managing technology manufacturing is the challenge of building a very tight team of a very diverse group of employees. In a software company, there’s always some sort of cultural gulf between engineering and sales one needs to attend to. But in a manufacturing company, one is additionally as dependent on the Princeton PhD in the lab as the technician on the factory floor. Then for low cost, the whole thing needs to be done lean, that is, without all the overhead and layers of management that high-margin tech companies tend to have. Werner had some very unique knowledge and experience with this. It’s a whole package of lifelong lessons (that was not always easy to convey to board members who spend a few hours a quarter at the company and have no operating experience in any business, let alone commodity manufacturing).

We built and ramped two complete state-of-the-art factories: a cell production factory (a semiconductor fab) and a panel assembly factory (which works more like a car-production factory). Up to this day, Nanosolar is the only entity on the planet capable of simply printing the semiconductor of a solar cell in a commercially meaningful way. It’s quite a piece of magic really. At present low levels of capacity, the advantage of that is still somewhat latent. But the distinctly superior capital efficiency that goes along with that is commercially more meaningful than ever before, in particular because since the 2008 credit crisis capital efficiency has become only more precious.

At Nanosolar we had a very strong culture focused on talent more than number of years of experience, and results more than process. We had almost no attrition over the years and long-term commitment played out in various kinds of ways including that many employees had stock vesting as far as 8 years out. (We may have overstepped a bit on that. Silicon Valley tradition is half that length.) We also had the policy of showing people the (building’s) exit when someone asked about ‘exit’.

During 2009, I enjoyed working with Bill Campbell, the secret coach in Silicon Valley. For any CEO, it is a privilege to have the same advisor as Steve Jobs was counting on for so many years. Bill was very impressed by our management and helped us reinforce our unique culture. When leaning towards something but finding it possibly a bit out there, it is very valuable to have an advisor be able to point to a relevant internal decisions at Apple or Google of similar thinking. One of Bill’s pieces of advice I may not have given sufficient attention: “It’s just that your venture investors (Benchmark Capital) would never have hired Steve Jobs if they had a chance to.”

In hindsight, signing up Benchmark Capital’s Bill Gurley, who served on our board for eight years, was one of the biggest mistakes we made. I could not agree more with Marc Andreessen’s take in a New Yorker profile:

We were always the anti-Benchmark,” Horowitz told me. “Our design was to not do what they did.” Horowitz is still mad that one Benchmark partner asked him, in front of his co-founders, “When are you going to get a real C.E.O.?” And that Benchmark’s best-known V.C., the six-feet-eight Bill Gurley, another outspoken giant with a large Twitter following, advised Horowitz to cut Andreessen and his six-million-dollar investment out of the company. Andreessen said, “I can’t stand him. If you’ve seen ‘Seinfeld,’ Bill Gurley is my Newman”—Jerry’s bête noire.

In June 2006, we announced that we had managed to close funding in an amount not done before by a solar company and were planning to use it to build a factory basically an order of magnitude larger than past solar factories. The capital raise was novel in size as well as approach in that it pioneered skipping the Valley’s late-stage VCs in favor of global hedge funds and family offices. The size of the planned factory was novel but representative of the not-your-grandfather’s-solar customer demand and growth shaping up in the end market. By not giving a timeline of how many years it would take to build a large factory based on new materials, some ended up believing that that’d happen overnight or within a year.

Renewable Energy Access: World’s Largest Solar Plant Planned in Bay Area;

San Jose Mercury News: Largest Solar Cell Factory Coming to Bay Area;

CNET: With hefty funding, solar start-up takes on big guns;

GlobeSt World’s largest solar plant planned in Bay Area

Energy and Capital, Sept 19, 2006

Thin Film-Solar’s Holy Grail

“Nanosolar owns the best-in-class thin-film technology.”

Globe and Mail, November 12, 2006

Nanosolar set for expected clean-tech boom

Shawn McCarthy in Canada’s national newspaper: “Veteran entrepreneur Martin Roscheisen — who studied engineering with Google founders Sergey Brin and Larry Page at Stanford University — founded Nanosolar with their backing four years ago and now has big production plans.”

The Economist, Nov 18, 2006

Green dreams

Editorial leader to the Nov 18th print edition

The Motley Fool, Dec 18, 2006

A Rising Sun?

“…might even allow Nanosolar to become the dominant player in the industry”

SF Chronicle, Dec 12, 2006 San Jose will have innovative solar plant

Plenty Magazine, March 17, 2007

Nanosolar: #1 of Green Energy Top 20

“Unique technology gives Nanosolar a huge jump on its competitors”

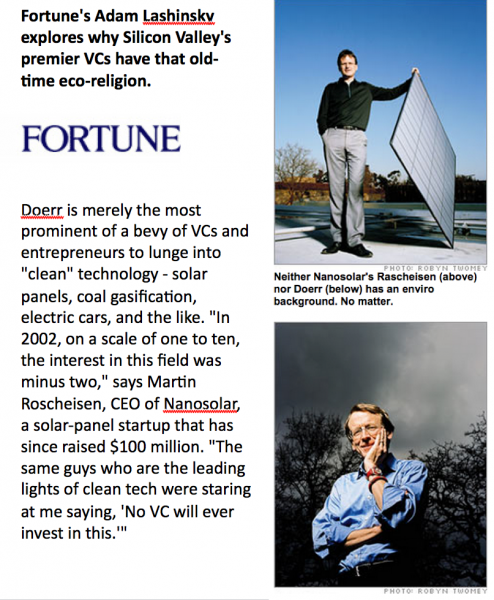

Fortune Magazine, April 10, 2007

The Jolly Green Bubble

“Silicon Valley’s premier VCs get eco-religious? Neither VC John Doerr nor entrepreneur Martin Roscheisen has a background in enviro.”

Earth2Tech, July 30, 2007

10 Questions for Nanosolar CEO

Earth2Tech’s widely read Q&A

Popular Science, Nov 12, 2007

Nanosolar: #1 Innovation of the Year 2007

Nanosolar named top innovation of the year.

The Guardian, Dec 29, 2007

Solar energy ‘revolution’ brings green power closer

“Nanosolar attacking the holy grail of renewable energy”

EDN, Jan 21, 2008

A Solar Panel On Every Building

“Nanosolar boast an impressive list of the world’s firsts”

Greentech Media, June 18, 2008

Nanosolar Creates Largest Thin-Film Tool

“If they’ve got that, they’ve got the world by the tail…”

In Sept 2008, the media got hold of the fact that six months earlier we had closed a strategic financing of $300 million. We had not planned to announce this at all actually — these types of news always only help competitors.

Venture Beat: Nanosolar outshines the competition with a $300M financing;

San Jose Mercury News: Thin-film solar firm Nanosolar says it has raised $300 million – “Largest amount of money raised by a solar start-up”

Silicon Alley Insider, January 24, 2009

VC Investing: Nanosolar took the top spot in 2008

USA Today, September 8, 2008

Energy Innovators: 4 creative solutions to energy problems

“Nanosolar one of the more exciting products in solar energy’s history”

Time Magazine, October 30, 2008

Best 50 Inventions 2008: Nanosolar

“Nanosolar a top 50 invention of the year”

Politico, February 25, 2009

Whither energy industry’s Bill Gates?

“Roscheisen has long had a penchant for all things green.”

In hindsight, the peak of exuberance in media reporting can presumably be marked when Popular Science named Nanosolar’s panel the #1 product innovation of the year — relegating into the #2 spot the new Apple iPhone. Not a single marketing person was working on our behalf while Apple truly has an army of public relations staff. While I could probably spend the rest of my life in a highly lucrative career in marketing by claiming that I did it — upending Steve Jobs — I’m afraid I can’t really claim I did anything for that. (The one time I had a chance to meet Steve Jobs we joked about that.) Clearly, there was something else going on, way out of our control. That said, the amount of innovation involved in our solar cell was truly something that Steve Jobs respected as meeting and exceeding that of his own company.

In September 2009, we hit a major milestone: We inaugurated our fully automated high-volume panel-assembly factory located close to our customers in Germany (image with state governor, Democratic candidate for chancellor):

The New York Times: Nanosolar pulls back the curtain on its technology;

Wired: Thin-Film Solar Startup Debuts With $4 Billion in Contracts;

PV-Tech: Printed PV: Nanosolar unveils 640MW utility-scale panel fab, high-efficiency CIGS cell production; Nanosolar remastered: An interview with company boss Martin Roscheisen

Inauguration video featuring key management that made it all happen:

The two fabs (cell and panel factories) were finally operating and product coming out for first substantial installations. This looked like this:

Despite production having commenced, we continued learning more about certain less well known idiosyncracies of the semiconductor we were using than we ever cared to learn about. I ended up having to order a full stop to production three more times. My personal reputation took it on the chin with the gotcha-playing blogosphere as a result. But I preferred that to shipping bad product.

Going for a novel semiconductor material implies an expected share of surprises of course. Still one would think that at a point in time where more than >$2B had been invested in companies working on that technology, on certain very basic attributes, not all of the world’s experts can be wrong. But we experienced several cases of that. Random high beta at way too late a stage.

It turns out there’s issues that tend to get investigated by research institutions and issues that don’t tend to get researched a lot. One of the biggest logic errors anyone tends to make is to confuse absence of evidence with evidence of absence. Very late it sunk in fully with us simply that no-one had ever put a CIGS panel into the sun and accurately checked it to be truly stable over time. Because that requires having a full product which no researcher has yet had.

Managing these setbacks was difficult in public communication in today’s media landscape now thoroughly dominated by daily beat bloggers often just playing games of Gotcha. When we had started production, we honestly communicated this; so how does one communicate a stop? It’s bloggers’ favorite game of petty gotcha’s (“you said this back then and now you say this”), which can be churned out fast, require no substantive understanding, yet generate the desired clicks. Fortunately, I do have a thick skin, and especially so for comments that lack any substance and are purely procedural. (In fact, I do even empathize with bloggers who generally have good intentions but simply are professionally in the tough spot of having to cover very complex industries with their click-based income model. Btw, based on how Internet media has evolved since 2000, I now find it advisable for startups to be completely off the blogosphere, which is what I’m doing now.)

Time wise, since our inception, Nanosolar had usually tracked 2-3 quarters behind our competitor Miasole, including later in production volume ramp. Some journalists criticized Nanosolar for that, not always with a fair understanding. While the product is essentially the same, the inside of the product is distinctly not. From the beginning, Nanosolar was shooting for far more aggressive inside targets: three times better semiconductor materials utilization than Miasole; one third the cost of their cell foil; a factor higher tooling productivity; etc. Benefits of such magnitude don’t just come out of nowhere for free. When Miasole “just” developed new tooling design, Nanosolar had to that plus develop completely new materials processes. When Miasole could rely on a known process, Nanosolar had to invent a completely new one. This put Nanosolar by design on a very different timeframe. All investors knew about it and had bought into it. Given expectations of a commoditizing industry, investing into a company that would achieve a more fundamental cost advantage is a good idea even if it takes longer to get there. Still it’s difficult to communicate this at times, and it became somewhat of an obsession of the press to track this. And it’s virtually impossible to accelerate on a moment’s notice when a board member sees a competitor filing to go public and suddenly feels we ought to as well.

Time wise, since our inception, Nanosolar had usually tracked 2-3 quarters behind our competitor Miasole, including later in production volume ramp. Some journalists criticized Nanosolar for that, not always with a fair understanding. While the product is essentially the same, the inside of the product is distinctly not. From the beginning, Nanosolar was shooting for far more aggressive inside targets: three times better semiconductor materials utilization than Miasole; one third the cost of their cell foil; a factor higher tooling productivity; etc. Benefits of such magnitude don’t just come out of nowhere for free. When Miasole “just” developed new tooling design, Nanosolar had to that plus develop completely new materials processes. When Miasole could rely on a known process, Nanosolar had to invent a completely new one. This put Nanosolar by design on a very different timeframe. All investors knew about it and had bought into it. Given expectations of a commoditizing industry, investing into a company that would achieve a more fundamental cost advantage is a good idea even if it takes longer to get there. Still it’s difficult to communicate this at times, and it became somewhat of an obsession of the press to track this. And it’s virtually impossible to accelerate on a moment’s notice when a board member sees a competitor filing to go public and suddenly feels we ought to as well.

As Nanosolar grew into a business with a heavy international and operational activities, one key mistake I made was to not sufficiently evolve the company’s board of directors. The individuals from the early-stage venture firms tend to be people with a good skill set at scouting out promising Bay-area startups. But as a company grows and the executive team matures through senior additions (and as the venture investors percentage of contributed capital shrinks to a small fraction — just 5% in our case), it is important to have a board of directors with deeper business operating, management, international, and industry experience. A real operating business and the world at large out there is just very different an animal than what a typical venture investor tends to get exposed to within the Silicon Valley horizon. By not ever really being in front of customers and suppliers and in touch with the industry at large, it’s actually quite difficult for a venture investor to scale with the company and maintain a good instinct about what’s going on. (I have actually found hedge-fund investors to be very much more in tune with the industry — that’s because they tend to know/visit/track the key other companies, etc.) Then board meetings tend to be a subtle thing and if someone has his instinct in odd places, it makes things difficult. The issue is simply also that during inevitably arising operating challenges, when steadiness is often the best prescription, a VC director with no operating experience tends to get weak in his knees overly quickly and often causes more damage than good. Then it is good to have other board members around to balance the group and point the board discussion onto what matters most. Unfortunately, a lot of damage can be caused by not having an effective board of directors.

As Nanosolar grew into a business with a heavy international and operational activities, one key mistake I made was to not sufficiently evolve the company’s board of directors. The individuals from the early-stage venture firms tend to be people with a good skill set at scouting out promising Bay-area startups. But as a company grows and the executive team matures through senior additions (and as the venture investors percentage of contributed capital shrinks to a small fraction — just 5% in our case), it is important to have a board of directors with deeper business operating, management, international, and industry experience. A real operating business and the world at large out there is just very different an animal than what a typical venture investor tends to get exposed to within the Silicon Valley horizon. By not ever really being in front of customers and suppliers and in touch with the industry at large, it’s actually quite difficult for a venture investor to scale with the company and maintain a good instinct about what’s going on. (I have actually found hedge-fund investors to be very much more in tune with the industry — that’s because they tend to know/visit/track the key other companies, etc.) Then board meetings tend to be a subtle thing and if someone has his instinct in odd places, it makes things difficult. The issue is simply also that during inevitably arising operating challenges, when steadiness is often the best prescription, a VC director with no operating experience tends to get weak in his knees overly quickly and often causes more damage than good. Then it is good to have other board members around to balance the group and point the board discussion onto what matters most. Unfortunately, a lot of damage can be caused by not having an effective board of directors.

In early 2010, one of my VC board members, who had had a latent presence for many prior years, came alive about his favorite topic of going public. He thought a competitor of ours would be valued at $3B after an IPO and we’d be behind. My opinion — that they would not be valued anywhere that highly and not even manage to complete the IPO and possibly be soon bankrupt anyway — exhibited a first disconnect. Another VC board member worked for a fund with atrocious performance on every other investment, leading them to oversell Nanosolar to their fund’s LPs as the investment that’s going to singularly return the entire fund. Another political problem. Then of course we certainly had plenty of operational issues that the team kept working through persistently at generally good progress. But some members on the board started zooming into our seasoned operations head and looking for silver bullets that could nail it all. Unfortunately, often there is no silver bullet and the only way to go is to keep shooting lead bullets as unglamorous as this might be. I backed our operations team and did not support firing and hiring VPs. I happened to be right in the end yet still lost my job. That’s of course the other action one can take in the find-the-silver-bullet mentality: Fire the CEO.

The New York Times, March 22, 2010: Executive Shakeup at Nanosolar

My ouster led to an incredible talent of a “professional” CEO being installed who proceeded to rapidly destroy massive amounts of shareholder equity. He lasted less than two years, during which time he managed to reduce the company’s price per share by a factor of 30. He instituted a 9-to-5 culture, with VPs precisely leaving minutes after the CEO, and many engineers at home at 5:30pm for the first time their spouses could remember. He staffed up the HR department to the size of the product reliabilty department while cutting down the latter to the size of one. (Given 20-year product warranties required, product reliability had always been a huge emphasis of ours but perhaps the new CEO got sick hearing from the guys.) The website now featured an EVP HR in the #2 spot right behind the CEO. Still the expanded HR didn’t keep more than 100 engineers leaving the company, with all of their specific knowledge acquired in many cases over 6-8 years. In particular, this included a lot of the key process engineers and tool designers, the core asset of the company. Engineers were stunned about the new management appearing to be in the belief that the tools the company had were ones that one sort of could just buy off-the-shelf somewhere, perhaps at Cosco. Meetings were held with suppliers where years worth of tightly guarded trade secret designs were just handed over. Several senior engineers quit in disgust over that. Still, the new management managed to report decent-sounding progress to the board and shareholders. The motto was that milestones were now being met. The problem was just this: the milestones were uninteresting and not suitable to create any equity value. By not having installed a better board, the company was now in the situation were bad management was supervised by a bad board. Very painful to observe.

As with any changes in CEO, the new team is in the position to tell all kinds of stories while the old is kept quiet through various legal agreements. Usually this is further exacerbated by the incoming execs being more highly trained in corporate politics and the art of “looking good” than the founding ones. I have been quite stunned by the amount of misrepresentation and straight lies some create while seeking to build their authority.

When I left in 2010, Nanosolar was in the enviable position of having close to $200 million in the bank and no debt. That’s a lucky position to be in, one that one has to thoroughly appreciate in this economic environment. As a founding CEO, one would stretch every dollar of that to make sure that no further financing is required. But with the hired CEO, the company’s long-held frugality went out of the window. Where using Skype worked just fine before, I now heard that a $100K video communication system had to be installed. $3-4m’s were spent on recruiting execs. Lots of retreats were held in enjoyable places. Lots of money got poured into stainless steel from new first-time suppliers.

Less than two years later, the money was all gone yet the company nowhere near profitable. While a scandal by itself, the response to it is even more so. When cash is getting low, as a founding CEO, one works really fast. Nanosolar would have tanked many times already if the founding team had not said ‘no way we are going to allow this to happen’. But as a hired CEO, one apparently also thinks of polishing one’s resume, retirement, and/or striking a deal on an inside-job financing (“let’s have the existing investors do an inside round at an arbitrarily low valuation; and you guys then refresh my CEO stake afterwards”).

Of course, the circumstances were different in 2012 than they were in 2008. But again, it’s a matter of skills, commitment, and creativity to come up with a solution and create equity value. These days, just because U.S. based high-beta investors have learned that greentech is real business, this does not mean that there is not plenty of capital in Asia ready to invest in it at very good terms. Gotta get on a plane for that though. Nanosolar in particular is highly admired for its innovation in many parts of Asia. China’s 5-year plan explicitly listed “printed CIGS” as a goal, and Nanosolar singularly owned that. Omitting any Asia based capital source in a fund raise, as Nanosolar’s hired team did in 2011, is not a very smart idea to say the least. And in terms of realizing a decent corporate exit for Nanosolar, following through on existing high strategic China interest in 2010/11 would have been it.

The future of greentech in Silicon Valley? It’s clear that we do not have the ecosystem in this region and this country to make this highly successful at this point. Regrettably. Because it’s such an important and large industry. And because the alternative vision is that of America being the place of $35K green-collar workers installing semiconductor products built by 6-digit-salaried engineers in China. (See more on my experience in China in my separate posting.)

Solar specifically will only keep growing even though there is not much to point to anywhere right now in technology that can be considered great business success. In 2008, I was being ridiculed for my goal of shipping solar panels at a price point of $1/W, ie. at a required manufacturing cost of 65 cents per Watt. The wisdom of the industry was that this was strictly unachievable. Some people thought I’m doing the industry some sort of disservice by gunning for that level and not seeking to ship a lot of volume before it’s clear how to do that. Well, only a few years later, the price points are now at just that targeted cost level. Entire solar power farms are now being built for as little as $1.5/Watt, and this includes the land and the fence around it and everything. That’s a third of what a nuclear power plant costs to build today (not including the subsidies that nuclear receives through subsidized insurance, etc.). It’s an amazing advance overall, and it was a privilege to have been part of the solar industry during this major change from niche to mainstream.

Pingback: bonus

Pingback: brain360 review

Pingback: payday loans