I am a tech entrepreneur, since 2013 focused on advancing the very foundation of tech at Diamond Foundry.

Born in Munich, Germany, as an Austrian citizen, I came to the Bay area to receive a PhD at Stanford University in computer science.

At Stanford, my intent was to work on AI as I had worked on emerging neural networks and been fascinated attending [backpropagation inventor] David Rumelhart’s research group meetings at Stanford during a summer. But it turned out there was no faculty in the area of neural networks at Stanford in computer science and, worse, the existing faculty was all the opposite, “symbolic systems” focused.

But it was right when Internet adoption started to take off. So I joined Terry Winograd’s group at Stanford, and enjoyed weekly research group meetings of five of us including Larry Page where we figured over time that it’d be good to try to use web links to create a better search engine.

Search was obviously big back then already but so was “group communication” as we called it initially, before “social” became the word to use. I focused on creating networks for Internet users to exchange ideas, sort of the earliest precursor of Facebook using email groups. Since Larry Page was adamant about not wanting to create a startup (and also explained me each week how bad advertising is), I recruited his brother and the engineer who had coded Backrub, the first version of Google, to create eGroups, which became one of the fastest growing consumer services in the late 1990s. Sequoia Capital funded us and I got my “MBA” from Michael Moritz in that way, who then served as Sequoia’s chairman for a long time.

After the dotcom bust, initially semi-retired after Yahoo! had purchased eGroups, I felt that there’s big industries, in particular energy, that could be transformed through a Silicon Valley type approach. Like making solar power ten times less expensive. So in 2002, I started Nanosolar and ran it for eight years until 2010 — as the longest serving CEOs in the solar industry back then.

Nanosolar was the first solar tech startup funded by American venture capital (Benchmark Capital) and became Silicon Valley’s solar flagship co as we were developing an ultra-low-cost solar cell and building two substantive high-tech fabs. I ran Nanosolar from zero to $2.1B in market value. Then I was forced out over our competitor Solyndra filing for an IPO ahead of us, and three years later, Nanosolar failed with inept leadership having been installed by investors.

In 2010, I adopted an embrace-don’t-compete attitude towards China and moved to Shanghai. I worked on creating a greentech park in Hu Jintao’s hometown and a battery company in China with the support of local investors and the government and gained some first-hand insight into how things work entrepreneurially on the ground over there. (Update: As of 2023, I still believe that trying to compete with China in materials tech is a rather bad idea.)

I keep trying to figure out the “high-beta tech economy” — an activity that tends to be as humbling as refreshing. I also find that stories we read and tell, in particular journalistic reporting, tend to succumb to “narrative fallacy”. So if this blog appears at times a bit non-linear, it may as well be closer to the truth.

I generally stay away from the tech conference circuit where CEOs or founders hang out with each other. (I do go where actual customers go.) I also do not take advisory roles and rarely if ever invest in startups. I prefer to be all in with my time on the business I’m actually in. (I led the first three rounds in my current company and invested in it seven times…)

Still through this blog, I am looking forward to occasionally share some perspective on things I find worth noting.

After working for a year on what today is called “big data” at the legendary Xerox PARC (where the graphical desktop UI, Ethernet, the laser printer were all invented), I started in the doctorate program in computer science at Stanford University. It turns out the security of a $1,600/month paycheck from the Stanford PhD program as well as the U.S. immigrant visa it affords (in addition to some great Stanford infrastructure) was a truly amazing place to learn about tech innovation and allow me to pursue my entrepreneurial inclination.

I joined Stanford Computer Science just around the time when the “World Wide Web” started to emerge out of a soup of prototypes and protocols. (Curiously back then, “interactive TV” was really the hot new thing in Silicon Valley, and the web thing was regarded somewhat like a better bicycle in the automotive industry…) I built the first group annotation system that worked right into the Mosaic browser and became familiar with every line of code that Marc Andreessen was writing over at NCSA.

At Stanford, I was part of Terry Winograd’s small group of five PhD candidates, which also included Larry Page whose work on search ended up becoming the business story of the century in hindsight. Things move along with a fairly slow yet concentrated calm in the setting of a PhD program, especially at a place like Stanford. One week the group discusses that web links are really unexploited territory for improving search in some way. Weeks pass and not much happens. Some code is written now and then. Sitting in an office that used to be that of the founders of Cisco one wonders now and then whether the truly big stuff may have already happened. Yet one thing holds: the longer-term effect of being on an exponential curve is easily underestimated at any moment of time!

While at Stanford in our group, Scott Hassan had written pretty much the entire first version of the Google search engine (Larry was not coding much). His code was just purely beautiful. Scott had also written the code for a service that would archive the messages of virtually every mailing list out there. I felt like the latter and Scott’s amazing engineering would be a great foundation to build a service that would host group communication more than just archiving it, and I connected with Scott about this and we decided to form a company around this — with Carl Page (Larry Page’s brother) being the third co-founder.

eGroups

eGroups was one of the first true social networks, before “social network” was a term. We called it somewhat more awkwardly “group communication” back then. I was the founding CEO with the early team consisting of Scott Hassan (now of Willow Garage), Carl Page (Larry Page’s brother), Ramu Yalamanchi (later founder of Hi5 Networks), and Alan Braverman (later founder of Xoom and Yammer).

With funding from Michael Moritz at Sequoia Capital, we went on a fast track to grow the service very aggressively. eGroups grew at a faster rate than any other Internet consumer service back then except for AOL’s ICQ chat service. We grew into the largest email hub on the Internet behind AOL in 1999/2000.

It was a pleasure working with Mike and Sequoia Capital. The very best investors are in an entirely different league than everyone else. They do things differently. Mike, for instance, didn’t even bother to engage an investor counsel to complete the financing. Just used the company’s and saved a lot of time and expense. (Moritz subsequently also invested in Larry’s company, Google — one of the best investments ever made.)

While riding the hyper growth rocket, we surely made our share of mistakes. Some of them stemmed from the crazy dotcom environment even though relatively speaking we managed to keep our feet on the ground and stay clear from a lot of its excesses. We tried hard building a real business with real revenue while competing against others who just focused on accumulating more users.

Monetizing all the users we had at eGroups turned out tough. We simply didn’t manage to crack that nut. So we decided to sell the company. eGroups was acquired in 2000 by Yahoo (subsequent to merging with our biggest competitor) when it had grown to approximately 50 million users. [c|net article: Yahoo buys eGroups in $450 million stock deal] Many of the key engineers ended up moving over to Google and built Google Groups there. Sending a billion email messages fast is not easy to develop and deploy and required rewriting a lot of fundamental software. There’s rumors that at the point of Yahoo acquisition, eGroups still had a copy of the source code of the Google search engine on its servers — but I can’t say.

While working on eGroups, I remember sensing some sort of possibility of a highly cohesive web based interaction network — sort of like Facebook is today. But that never materialized as we were running around trying to hire people and navigate through an investment bubble. My biggest regret in hindsight is that I didn’t resist our board in hiring “experienced” engineering managers; it would have been better for the founders to continue to be hard-core engineering leads as opposed to transforming into crappy general managers. Silicon Valley has gotten smart on that over the past decade. These days, Facebook shows how much bigger and more meaningful a business we might have had a chance to grow into.

TradingDynamics

Stanford professor Yoav Shoham pinged me one day to join him in on creating a company that’s eBay for enterprises. I became the co-founding CTO and developed the initial plans and designs with Yoav. When both eGroups and TradingDynamics received initial funding during the same week, I chose to focus on eGroups (see above). Still, 15 months later, TradingDynamics got acquired for the value of the GDP of an African country. [c|net article: Ariba completes $720 million TradingDynamics buy] More high beta followed. Down to zero value for some years. Then ten years later, TradingDynamics is now routinely used for all component sourcing in large corporations such as IBM.

FindLaw

I co-founded FindLaw with two Harvard/Stanford law graduates, Tim Stanley and Stacy Stern. FindLaw grew into the largest legal website. Our first funding came in the form of a customer paying in advance for a year’s of service. Acquired in 2001 by Thomson Reuters. [Articles: West Group acquires FindLaw; early NY Times article about FindLaw] It takes some very dedicated founders and being early on an investment wave to bootstrap a business — but can be a lot of fun and lead to some very solid value.

Tank Hill Projects

In 2000, I teamed up with Mark Pincus (now of Zynga), to create an incubator for launching companies developed by us. But after raising $10m and hiring 50 people (including a Ukrainian development team), we concluded wrong time, wrong place, wrong approach and chose to return the money to the investors. Few investors see their money back without asking, so this actually set a good example for people trusting us to not keep sitting on their money if we don’t find a good use for it.

Nanosolar was a high-risk entrepreneurial foray into the world of energy, semiconductors, and manufacturing, which I made to make a difference on making green energy broadly affordable. I ended up mobilizing a Google quality team and $500+ million in capital from blue-chip investors for one of the industry’s most serious efforts to make a 10x difference in solar power technology.

The plan we had was ambitious and included reinventing virtually every aspect of a solar electricity cell, applying novel processes to novel substrates with novel tooling. The goal was to arrive at a highly efficient solar cell composed of cheap Aluminum foil with a thin film of a semiconductor printed on top of it (as well as 15 other low-cost ancillary layers). No other company had ever replaced semiconductor processing with simple printing. No efficient solar cell had ever been produced based on the cheapest of all conductive foils.

It took a torturous amount of perseverance, determination, and outside support to get all that innovation working. In the end, our team did manage to deliver numerous against-all-odds technological breakthroughs and translate them into two dozen completely new manufacturing processes and tooling designs and implement them all the way in two state-of-the-art fabs, which ramped over time to >90% end-to-end yield. World-record efficiencies were achieved. The world’s largest utility backed us with a binding $1B purchase contract. The smartest investors piled in. And the list goes on.

Yet it ultimately failed commercially. Like essentially every other solar tech co it turns out. (Sadly, this became an industry where no tech co truly succeeded and only businesses based on financial engineering are now seeing some success.) As usual, whoever does anything makes mistakes, and we made plenty of mistakes. But so do people in many startups that succeed greatly.

In hindsight, I would not touch a business again with any of these three attributes — they simply make it too hard to succeed as a startup: 1. Long product reliability testing required. 2. Many production steps with statistical yields. 3. No China story upfront. The solar panel business had them all. As a startup, one needs fast development cycles, and then fast access to customer dollars once a product is developed. Observing a solar field installation for a year to prove a product keeps performing is not part of that. (Btw, other industries like battery technology are not at all better on that, and thus similarly unsuited for startups in my view.)

More detailed history on Nanosolar:

With my initial entrepreneurial success in Internet software giving me the freedom to do whatever I thought is most worthwhile, in 2002, I decided that it would be meaningful if I’d be able to bring to bear a Silicon Valley type approach to making a difference on difficult technological challenges in the area of sustainable / green energy. I picked the then rather uncharted frontier of solar power. Product and factory cost were holding back solar in a major way from its obvious potential. The question was how to make a big leap of a difference on cost and capital efficiency.

Various inventors had been pursuing novel semiconductor process technologies but few did much to turn this into real products. There was a lot of pioneering science out there but little really intense, focused commercial development. We set out to change that and go after the most promising route in a commercially meaningful and intense way. It did in fact turn out to be difficult, if ultimately in unexpected ways.

Pursuing the endeavor involved basically two grand bets — whether it’s possible to achieve technological breakthrough in a completely new area using a certain style of approaching things; and whether it’s possible to finance such an effort with the hundreds of millions of dollars it requires.

The technological grand experiment — being able to master incredible innovation in green energy technology — basically worked out fine. Smart engineers put behind the right goals and equipped with good funding can truly move mountains and, with intense work, prove all sorts of nay-sayers wrong (and there’s plenty of them at any time). It is always difficult for people at the outside to fairly judge what someone is making under the hood of commercial secrecy — blog and press coverage fluctuated somewhat randomly from exuberant to fatalistic. But the benchmarking we did with CEOs of other leading manufacturers were much clearer feedback: Whenever we showed one of them what we have under the hood (and we did not mind doing that), their jaws would usually drop to the floor by the end of the tour. The European ones tended to say that our team had accomplished in 6 years what their heavily subsidized groups did not get anywhere close to achieving in 20 years. That was the crux of the matter: Huge acceleration and leaps are in fact possible in greentech with a startup style of research and development, and untapped opportunities abound left and right in science based innovations pursued with a startup mindset.

The other grand experiment was whether it’d work to expand the realm and horizon of high-beta investors into greentech — and associated with this: 7-year development cycles, seriously international business, global manufacturing, the risk of blow-ups that kill people and necessitate large-area evacuations, and a lot of other big-boys stuff. Solar technology had been completely uninvestible in Silicon Valley and elsewhere. In 2002, no fund had ever invested in a solar company. Kleiner Perkins was contemplating greentech but not committed to it yet. Their feedback to us back then was: “What is the value proposition of solar power?” (after a pitch on printed solar versus other technologies). A Nobel laureate venture partner at a leading other firm suggested “We don’t do that in Silicon Valley — try go and speak with GE.” Planning to do manufacturing was not something anyone could remember having heard of lately. (“Last time anyone manufactured here must have been more than a decade ago.”) Venture investors had clear screening criterias which excluded anything energy, anything green, and in particular anything manufacturing. Today many investors are gone and effectively back to these criteria, possibly for good reasons. (Still overall, not the result that optimizes the common good in the best way — see also Why Facebook is killing Silicon Valley.)

Still in 2002 I felt we ought to be able to bring Silicon Valley type technological and company-building capabilities to this important industry. Given our non-China location, it was clear that our value would be in innovation and we would have to go very much for a plan of developing the ultimate solar electricity panel with maximum conceivable cost and capital efficiency. Nothing else would have been investible here (and I did try). We figured out what kind of a plan this would need to be technically–a plan that changed very little over ten years. (And once on that track, it was rather difficult to soften this towards a not-quite-as-radical-low-cost but faster-to-market approach.)

When one is targeting an entire factor of a cost reduction on a manufactured product with many components, it does not suffice to just deliver a massive innovation on one component — because improving one 15% component by infinity basically just makes that 15% difference overall. So this quickly becomes an all-out effort to develop completely new processes and designs for every component all the way, with hundreds of engineers at the company and its suppliers. We were fortunate to be in the historically unique position to do just that. (Here’ the detailed technical white paper. The really fun — technical — stuff I’m afraid I can’t discuss here. I can only say there’s been amazing innovation at every level.) With enough capital and years of persistence, the right team can keep hammering out the details and deliver some pretty incredible innovation on some very audacious goals. And that’s what we did.

I got Nanosolar going with the help of a few Internet angel-investor friends of mine, including Sunil Paul, Mark Pincus (who I had co-run a company with), Reid Hoffman (who I first met when both of us worked at PARC in the late 80s) as well as Sergey Brin and Larry Page (who I went to school with). The latter put in a marginal amount but back then they were not even liquid with their Google stock and it was a first investment for them. The quality of these initial supporters ultimately led to the fact that we became the first company to obtain funding from venture capital investors. (Benchmark Capital and USVP ended up being Nanosolar’s initial venture investor. USVP exited at a profit of a small multiple in 2005 when I shifted the company’s printable solar cell development from a highly instable and expensive organic semiconductor to the relatively a lot more established CIGS semiconductor, a move that they did not subscribe to. The other organic PV companies there were soon went out of business, so that was a bullet dodged early!) Btw, many of the early investors did actually very well with their investment — they all had a chance in 2008 to take some of their investment off the table at a 125x increase in share price, that is, if someone sold only 20% of their shares at that 125x, this still delivered a 25x overall return even if one completely discounts the remaining 80% holding. Some of the later strategic investors bought supply optionality which was important to them beyond the value of their investment. (Plus Goldman Sachs did the due diligence for them.)

Without being particularly interested in it and certainly not actively pursuing it, we received a lot of media interest. We were always amused when people thought that we had an entire team of public relations people on staff at Nanosolar. In fact we had none. We were way too frugal for that. (Investors often called us the most frugal company with the most capital they’ve ever seen.) This approach worked for many years except later when media sentiment turned on everything including the entire industry. Initially media interest centered around Internet entrepreneurs/investors attacking a completely new industry.

The New York Times, June 19, 2003 $6.5 Million Being Invested in a Venture on Solar Cells The NY Times first reports about the formation of Nanosolar: “Nanosolar is seen as a harbinger because of the strong pedigree of the venture capital firms and the track record of its chief executive and co-founder, R. Martin Roscheisen”

USA Today, CNN, April 26, 2004 Clean-tech firms attract growing share of venture dollars An article syndicated by the Associated Press in major publications around the world reports about Nanosolar “turning heads in Silicon Valley” with a new solar ink.

San Jose Mercury News, Aug 15th 2004 World events spark interest in solar cell energy start-ups The lead article in the Silicon Valley’s Mercury news: “Nanosolar’s Roscheisen embodies the new interest among Silicon Valley veterans in solar.”

Fast Company, Nov 30, 2004 Green Power “The time may finally have come for these champions of on-the-verge technologies.”; “Roscheisen funded the company’s early research himself, and with angel investment from friends such as the founders of Google, but eventually he decided to raise $6.5 million in venture capital.”

History Channel, Dec 30, 2004 Modern Marvels: Energy Technology [Video] First public footage of Nanosolar’s prototype coater in a History Channel episode on “staving off the looming global energy crisis”.

National Geographic, Aug 2005 Powering the Future A cover story in the National Geographic about interest in alternative forms of energy including Nanosolar.

Motley Fool, Jan 20, 2006 Is the Price of Power Getting You Down? A first mention in the Motley Fool: “Unfortunately, ordinary folks can’t invest in it yet.”

Business Week, June 20, 2006 Green Growth Areas for Entrepreneurs “When technology entrepreneur Martin Roscheisen was looking for the next big thing in 2001, the Internet wasn’t part of his plans. Instead, he looked to the field of solar photovoltaics (PV), specifically at work being done by a small research company named Unisun Corp. Roscheisen recruited one of Unisun’s main researchers, and sought funding in California’s Silicon Valley. The pitch: thin-film solar cells that could be produced for less, more efficiently, and on a significantly larger scale than standard solar paneling.”

Some of the coverage above implied hopeful expectations about how quickly this potential impact would materialize. In these early years, this was in part due to the writers not understanding that putting atoms on top of each other is very different than an IT product where one assembles some components; in part due to my not taking particular care of making that clear. In a sense, I was more concerned about making payroll — already twice we had gotten to within hours of bouncing checks — so enthusiastic press coverage was surely welcome if it builds some more general support for this new area.

The crux about Nanosolar was to make solar production more capital efficient in particular. It’s difficult to see a viable business or industry if it costs a dollar in capital expenditure to generate a dollar in revenue. Capital efficiency continues to be the Achilles heel of the solar industry, and Nanosolar planned to get (and did get) a factor ahead of everyone in this area.

Even though a far more capital efficient technology, our capital requirements were still stiff. It’s developing a completely new semiconductor process and tooling to produce it. So we constantly had to make sure we had sufficient capital. Nothing worse than a fabulous engineering effort that runs out of money. And fortunately we had gotten the timing just right. The energy macro was taking off. Kleiner Perkins had made a decisive public commitment, and even we did not end up working with them, their signaling is read by a lot of investors. Around 2005 I remember being at an increasing number of dinners with pension funds and other large “LP” investors asking me which venture fund I know who invest in greentech. Predictably, soon basically every VC firm on the planet had at least one partner dedicated to greentech. It was the luck of a rising tide in which Nanosolar ended up having an unfair advantage due to being early. (This also led to a lot of envy by others as well. Of course, the envious ones tend to forget that someone else prepared the road for them in the first place.)

With our early start, we were able to scoop up an immense pool of talent. Our hiring was extremely selective, focused on raw talent and curiosity and drive more than experience. We’ve always found that issues and challenges change way too fast during the course of development, that it’s best addressed by all-around smart people whose curiosity has a burning intensity capable of making things work that others wouldn’t even try. I had seen this earlier in the Internet space in the late 90s where lots of companies got started but few had typically more than two or three truly great engineers — and then Google came along and had a complete pool of truly great ones. One of the things I was most proud of at Nanosolar is that we clearly had this pool of dozens and dozens of engineers each of which of star quality. Even the consultants we had working for us (under NDA and other IP protection) included individuals such as Gronet and Basol, who later founded Solyndra and Solopower respectively. (Btw, as for other companies abusing taxpayer funds, at least I am on the public record and also here for warning of the latter to happen. I mean this was a company whose solar product had half of the semiconductor material not in line of sight with the sun.)

The quality of our effort and early lead also exhibited in the quality of the partners we were able to engage with. The world’s largest utility ended up backing us effectively with their balance sheet — they signed a $B worth of legally binding purchases — and the CEO of the largest developer of large solar power plants in the world spent personally hundreds of hours assisting us with product definition and roll-out. It was truly wonderful.

Raising capital was never as easy as some may think given the fact that we raised half a billion in development funds. For what we were trying to do, it basically required coming up with entirely new ways of raising capital. That took a lot of creativity and effort which many others failed at. It’s one thing to raise capital if there exist funds focused on your company’s industry/stage/product; it’s another thing if there don’t. We never worked with any investment bank; pretty clear they would have failed. These were pioneering forms of raising capital. Our 2006 and 2008 financings were each the largest of any private tech company on the planet in each of these years. “Up” rounds every single time even though we often did not have much to show for yet. The experiential upside of not being able to just drive up and down Menlo Park for fund raising was an assortment of memorable meetings — such as a Sunday afternoon tea in Kuwait with Mr. Oil (OPEC’s Secretary General), a lunch at the city of London’s very much most elite members’ lunch club (where my lunch partner discussed Russian capital “that desires to become legitimized” at our table which was within hearing distance of each of those of the Chairmen of Goldman Intl and Exxon); etc.

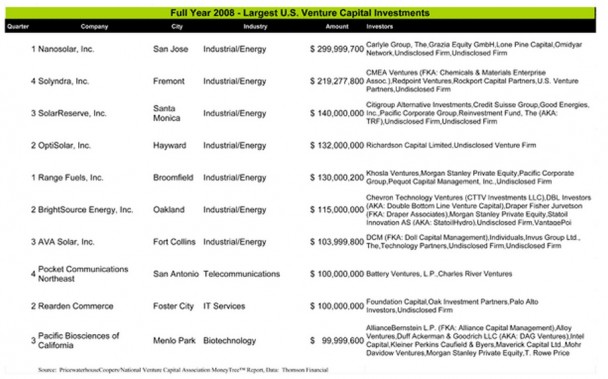

Above: Largest venture financings in 2008 is dominated by solar companies, with Nanosolar at #1.

Above: All-time (1970 thru 2009) largest venture financings as of 2009. Three greentech companies, including Nanosolar. Just two years later, this list would look completely different with ‘social media’ companies all over.

I was Nanosolar’s Chairman & Chief Executive Officer from the company’s inception in 2002 through commenced “normal production” in 2010. With our industry flagship status, I got invited to every world leader and political hob-nobbing conference on the planet; I never hesitated a second to decline them all. I was always highly suspicious of startup CEOs going to certain conferences; I would not ever invest in any such companies. Instead I myself enjoyed spending my time in the details of managing the technology development, architecting the product and process with the team. What I really enjoy most is to be able to show up at work and have really smart, really motivated engineers there, cranking on something magic.

In lockstep with a very experienced manufacturing executive, Werner Dumanski, we managed to go from the “against-all-odds” nanoscience research to manufacturing process development, production tooling development, product development including some rather challenging work on product reliability and certification.

Werner had previously run all of IBM’s $4B storage-disk operations, with 14,000 employees in his organization. It’s an example of what’s great about Silicon Valley. IBM at one point noted that one of their storage-disk factories in Germany did a far better job than its team in San Jose which had invented the very technology. Puzzled about that, they asked the leader of that group to report to work in San Jose the next Monday. That was Werner. Soon the U.S. operation was in shape: high yield and lean. And Werner ended up managing all of manufacturing at IBM. Now in Silicon Valley, he joined us at Nanosolar, initially with a staff of zero and a $1B smaller budget. Werner had all the attributes of a “level-5 leader” and I backed him fully all the way to the extent of my own ouster instead (which did not avoid his in the end though).

A unique aspect to managing technology manufacturing is the challenge of building a very tight team of a very diverse group of employees. In a software company, there’s always some sort of cultural gulf between engineering and sales one needs to attend to. But in a manufacturing company, one is additionally as dependent on the Princeton PhD in the lab as the technician on the factory floor. Then for low cost, the whole thing needs to be done lean, that is, without all the overhead and layers of management that high-margin tech companies tend to have. Werner had some very unique knowledge and experience with this. It’s a whole package of lifelong lessons (that was not always easy to convey to board members who spend a few hours a quarter at the company and have no operating experience in any business, let alone commodity manufacturing).

We built and ramped two complete state-of-the-art factories: a cell production factory (a semiconductor fab) and a panel assembly factory (which works more like a car-production factory). Up to this day, Nanosolar is the only entity on the planet capable of simply printing the semiconductor of a solar cell in a commercially meaningful way. It’s quite a piece of magic really. At present low levels of capacity, the advantage of that is still somewhat latent. But the distinctly superior capital efficiency that goes along with that is commercially more meaningful than ever before, in particular because since the 2008 credit crisis capital efficiency has become only more precious.

At Nanosolar we had a very strong culture focused on talent more than number of years of experience, and results more than process. We had almost no attrition over the years and long-term commitment played out in various kinds of ways including that many employees had stock vesting as far as 8 years out. (We may have overstepped a bit on that. Silicon Valley tradition is half that length.) We also had the policy of showing people the (building’s) exit when someone asked about ‘exit’.

During 2009, I enjoyed working with Bill Campbell, the secret coach in Silicon Valley. For any CEO, it is a privilege to have the same advisor as Steve Jobs was counting on for so many years. Bill was very impressed by our management and helped us reinforce our unique culture. When leaning towards something but finding it possibly a bit out there, it is very valuable to have an advisor be able to point to a relevant internal decisions at Apple or Google of similar thinking. One of Bill’s pieces of advice I may not have given sufficient attention: “It’s just that your venture investors (Benchmark Capital) would never have hired Steve Jobs if they had a chance to.”

In hindsight, signing up Benchmark Capital’s Bill Gurley, who served on our board for eight years, was one of the biggest mistakes we made. I could not agree more with Marc Andreessen’s take in a New Yorker profile:

We were always the anti-Benchmark,” Horowitz told me. “Our design was to not do what they did.” Horowitz is still mad that one Benchmark partner asked him, in front of his co-founders, “When are you going to get a real C.E.O.?” And that Benchmark’s best-known V.C., the six-feet-eight Bill Gurley, another outspoken giant with a large Twitter following, advised Horowitz to cut Andreessen and his six-million-dollar investment out of the company. Andreessen said, “I can’t stand him. If you’ve seen ‘Seinfeld,’ Bill Gurley is my Newman”—Jerry’s bête noire.

In June 2006, we announced that we had managed to close funding in an amount not done before by a solar company and were planning to use it to build a factory basically an order of magnitude larger than past solar factories. The capital raise was novel in size as well as approach in that it pioneered skipping the Valley’s late-stage VCs in favor of global hedge funds and family offices. The size of the planned factory was novel but representative of the not-your-grandfather’s-solar customer demand and growth shaping up in the end market. By not giving a timeline of how many years it would take to build a large factory based on new materials, some ended up believing that that’d happen overnight or within a year.

Energy and Capital, Sept 19, 2006 Thin Film-Solar’s Holy Grail “Nanosolar owns the best-in-class thin-film technology.”

Globe and Mail, November 12, 2006 Nanosolar set for expected clean-tech boom Shawn McCarthy in Canada’s national newspaper: “Veteran entrepreneur Martin Roscheisen — who studied engineering with Google founders Sergey Brin and Larry Page at Stanford University — founded Nanosolar with their backing four years ago and now has big production plans.”

The Economist, Nov 18, 2006 Green dreams Editorial leader to the Nov 18th print edition

The Motley Fool, Dec 18, 2006 A Rising Sun? “…might even allow Nanosolar to become the dominant player in the industry”

“Unique technology gives Nanosolar a huge jump on its competitors”

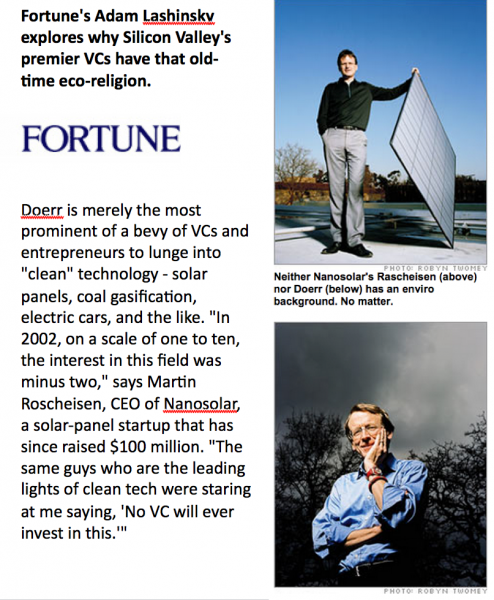

Fortune Magazine, April 10, 2007 The Jolly Green Bubble “Silicon Valley’s premier VCs get eco-religious? Neither VC John Doerr nor entrepreneur Martin Roscheisen has a background in enviro.”

In Sept 2008, the media got hold of the fact that six months earlier we had closed a strategic financing of $300 million. We had not planned to announce this at all actually — these types of news always only help competitors.

In hindsight, the peak of exuberance in media reporting can presumably be marked when Popular Science named Nanosolar’s panel the #1 product innovation of the year — relegating into the #2 spot the new Apple iPhone. Not a single marketing person was working on our behalf while Apple truly has an army of public relations staff. While I could probably spend the rest of my life in a highly lucrative career in marketing by claiming that I did it — upending Steve Jobs — I’m afraid I can’t really claim I did anything for that. (The one time I had a chance to meet Steve Jobs we joked about that.) Clearly, there was something else going on, way out of our control. That said, the amount of innovation involved in our solar cell was truly something that Steve Jobs respected as meeting and exceeding that of his own company.

In September 2009, we hit a major milestone: We inaugurated our fully automated high-volume panel-assembly factory located close to our customers in Germany (image with state governor, Democratic candidate for chancellor):

Inauguration video featuring key management that made it all happen:

The two fabs (cell and panel factories) were finally operating and product coming out for first substantial installations. This looked like this:

Despite production having commenced, we continued learning more about certain less well known idiosyncracies of the semiconductor we were using than we ever cared to learn about. I ended up having to order a full stop to production three more times. My personal reputation took it on the chin with the gotcha-playing blogosphere as a result. But I preferred that to shipping bad product.

Going for a novel semiconductor material implies an expected share of surprises of course. Still one would think that at a point in time where more than >$2B had been invested in companies working on that technology, on certain very basic attributes, not all of the world’s experts can be wrong. But we experienced several cases of that. Random high beta at way too late a stage.

It turns out there’s issues that tend to get investigated by research institutions and issues that don’t tend to get researched a lot. One of the biggest logic errors anyone tends to make is to confuse absence of evidence with evidence of absence. Very late it sunk in fully with us simply that no-one had ever put a CIGS panel into the sun and accurately checked it to be truly stable over time. Because that requires having a full product which no researcher has yet had.

Managing these setbacks was difficult in public communication in today’s media landscape now thoroughly dominated by daily beat bloggers often just playing games of Gotcha. When we had started production, we honestly communicated this; so how does one communicate a stop? It’s bloggers’ favorite game of petty gotcha’s (“you said this back then and now you say this”), which can be churned out fast, require no substantive understanding, yet generate the desired clicks. Fortunately, I do have a thick skin, and especially so for comments that lack any substance and are purely procedural. (In fact, I do even empathize with bloggers who generally have good intentions but simply are professionally in the tough spot of having to cover very complex industries with their click-based income model. Btw, based on how Internet media has evolved since 2000, I now find it advisable for startups to be completely off the blogosphere, which is what I’m doing now.)

Time wise, since our inception, Nanosolar had usually tracked 2-3 quarters behind our competitor Miasole, including later in production volume ramp. Some journalists criticized Nanosolar for that, not always with a fair understanding. While the product is essentially the same, the inside of the product is distinctly not. From the beginning, Nanosolar was shooting for far more aggressive inside targets: three times better semiconductor materials utilization than Miasole; one third the cost of their cell foil; a factor higher tooling productivity; etc. Benefits of such magnitude don’t just come out of nowhere for free. When Miasole “just” developed new tooling design, Nanosolar had to that plus develop completely new materials processes. When Miasole could rely on a known process, Nanosolar had to invent a completely new one. This put Nanosolar by design on a very different timeframe. All investors knew about it and had bought into it. Given expectations of a commoditizing industry, investing into a company that would achieve a more fundamental cost advantage is a good idea even if it takes longer to get there. Still it’s difficult to communicate this at times, and it became somewhat of an obsession of the press to track this. And it’s virtually impossible to accelerate on a moment’s notice when a board member sees a competitor filing to go public and suddenly feels we ought to as well.

As Nanosolar grew into a business with a heavy international and operational activities, one key mistake I made was to not sufficiently evolve the company’s board of directors. The individuals from the early-stage venture firms tend to be people with a good skill set at scouting out promising Bay-area startups. But as a company grows and the executive team matures through senior additions (and as the venture investors percentage of contributed capital shrinks to a small fraction — just 5% in our case), it is important to have a board of directors with deeper business operating, management, international, and industry experience. A real operating business and the world at large out there is just very different an animal than what a typical venture investor tends to get exposed to within the Silicon Valley horizon. By not ever really being in front of customers and suppliers and in touch with the industry at large, it’s actually quite difficult for a venture investor to scale with the company and maintain a good instinct about what’s going on. (I have actually found hedge-fund investors to be very much more in tune with the industry — that’s because they tend to know/visit/track the key other companies, etc.) Then board meetings tend to be a subtle thing and if someone has his instinct in odd places, it makes things difficult. The issue is simply also that during inevitably arising operating challenges, when steadiness is often the best prescription, a VC director with no operating experience tends to get weak in his knees overly quickly and often causes more damage than good. Then it is good to have other board members around to balance the group and point the board discussion onto what matters most. Unfortunately, a lot of damage can be caused by not having an effective board of directors.

In early 2010, one of my VC board members, who had had a latent presence for many prior years, came alive about his favorite topic of going public. He thought a competitor of ours would be valued at $3B after an IPO and we’d be behind. My opinion — that they would not be valued anywhere that highly and not even manage to complete the IPO and possibly be soon bankrupt anyway — exhibited a first disconnect. Another VC board member worked for a fund with atrocious performance on every other investment, leading them to oversell Nanosolar to their fund’s LPs as the investment that’s going to singularly return the entire fund. Another political problem. Then of course we certainly had plenty of operational issues that the team kept working through persistently at generally good progress. But some members on the board started zooming into our seasoned operations head and looking for silver bullets that could nail it all. Unfortunately, often there is no silver bullet and the only way to go is to keep shooting lead bullets as unglamorous as this might be. I backed our operations team and did not support firing and hiring VPs. I happened to be right in the end yet still lost my job. That’s of course the other action one can take in the find-the-silver-bullet mentality: Fire the CEO.

My ouster led to an incredible talent of a “professional” CEO being installed who proceeded to rapidly destroy massive amounts of shareholder equity. He lasted less than two years, during which time he managed to reduce the company’s price per share by a factor of 30. He instituted a 9-to-5 culture, with VPs precisely leaving minutes after the CEO, and many engineers at home at 5:30pm for the first time their spouses could remember. He staffed up the HR department to the size of the product reliabilty department while cutting down the latter to the size of one. (Given 20-year product warranties required, product reliability had always been a huge emphasis of ours but perhaps the new CEO got sick hearing from the guys.) The website now featured an EVP HR in the #2 spot right behind the CEO. Still the expanded HR didn’t keep more than 100 engineers leaving the company, with all of their specific knowledge acquired in many cases over 6-8 years. In particular, this included a lot of the key process engineers and tool designers, the core asset of the company. Engineers were stunned about the new management appearing to be in the belief that the tools the company had were ones that one sort of could just buy off-the-shelf somewhere, perhaps at Cosco. Meetings were held with suppliers where years worth of tightly guarded trade secret designs were just handed over. Several senior engineers quit in disgust over that. Still, the new management managed to report decent-sounding progress to the board and shareholders. The motto was that milestones were now being met. The problem was just this: the milestones were uninteresting and not suitable to create any equity value. By not having installed a better board, the company was now in the situation were bad management was supervised by a bad board. Very painful to observe.

As with any changes in CEO, the new team is in the position to tell all kinds of stories while the old is kept quiet through various legal agreements. Usually this is further exacerbated by the incoming execs being more highly trained in corporate politics and the art of “looking good” than the founding ones. I have been quite stunned by the amount of misrepresentation and straight lies some create while seeking to build their authority.

When I left in 2010, Nanosolar was in the enviable position of having close to $200 million in the bank and no debt. That’s a lucky position to be in, one that one has to thoroughly appreciate in this economic environment. As a founding CEO, one would stretch every dollar of that to make sure that no further financing is required. But with the hired CEO, the company’s long-held frugality went out of the window. Where using Skype worked just fine before, I now heard that a $100K video communication system had to be installed. $3-4m’s were spent on recruiting execs. Lots of retreats were held in enjoyable places. Lots of money got poured into stainless steel from new first-time suppliers.

Less than two years later, the money was all gone yet the company nowhere near profitable. While a scandal by itself, the response to it is even more so. When cash is getting low, as a founding CEO, one works really fast. Nanosolar would have tanked many times already if the founding team had not said ‘no way we are going to allow this to happen’. But as a hired CEO, one apparently also thinks of polishing one’s resume, retirement, and/or striking a deal on an inside-job financing (“let’s have the existing investors do an inside round at an arbitrarily low valuation; and you guys then refresh my CEO stake afterwards”).

Of course, the circumstances were different in 2012 than they were in 2008. But again, it’s a matter of skills, commitment, and creativity to come up with a solution and create equity value. These days, just because U.S. based high-beta investors have learned that greentech is real business, this does not mean that there is not plenty of capital in Asia ready to invest in it at very good terms. Gotta get on a plane for that though. Nanosolar in particular is highly admired for its innovation in many parts of Asia. China’s 5-year plan explicitly listed “printed CIGS” as a goal, and Nanosolar singularly owned that. Omitting any Asia based capital source in a fund raise, as Nanosolar’s hired team did in 2011, is not a very smart idea to say the least. And in terms of realizing a decent corporate exit for Nanosolar, following through on existing high strategic China interest in 2010/11 would have been it.

The future of greentech in Silicon Valley? It’s clear that we do not have the ecosystem in this region and this country to make this highly successful at this point. Regrettably. Because it’s such an important and large industry. And because the alternative vision is that of America being the place of $35K green-collar workers installing semiconductor products built by 6-digit-salaried engineers in China. (See more on my experience in China in my separate posting.)

Solar specifically will only keep growing even though there is not much to point to anywhere right now in technology that can be considered great business success. In 2008, I was being ridiculed for my goal of shipping solar panels at a price point of $1/W, ie. at a required manufacturing cost of 65 cents per Watt. The wisdom of the industry was that this was strictly unachievable. Some people thought I’m doing the industry some sort of disservice by gunning for that level and not seeking to ship a lot of volume before it’s clear how to do that. Well, only a few years later, the price points are now at just that targeted cost level. Entire solar power farms are now being built for as little as $1.5/Watt, and this includes the land and the fence around it and everything. That’s a third of what a nuclear power plant costs to build today (not including the subsidies that nuclear receives through subsidized insurance, etc.). It’s an amazing advance overall, and it was a privilege to have been part of the solar industry during this major change from niche to mainstream.

In mid 2010, I booked a one-way flight to China to learn more about things work over there. Motto: Embrace, don’t compete. I ended up spending much of 2010 and 2011 in various parts of China, getting involved with the government in creating a “green energy tech park” in the hometown of President Hu and teaming up with a Chinese entrepreneur to start a new grid storage business. For the latter, we received funding from one of the top Chinese investors. (And that one, within 24 hrs of signing the initial term sheet, got us in front of a regional secretary who gave us land, loan, facility, and an initial customer.)

Much like Silicon Valley has an ecosystem for successful Internet startups, I experienced China having an ecosystem for successful greentech companies. Ecosystems are about many elements but they tend to be finely tuned and subtle yet the whole can reach amazing effectiveness. One general aspect to the China ecosystem is competent government officials, carefully filtered over the years in their effectiveness of knowing how to get things done. (The untold story behind the Solyndra disaster in the U.S. is that it’s 24-year-olds who worked through these government decisions…) Usually engineers by training, in China, many of the very brightest graduates go into government each year. I have had conversations with senior government officials about greentech manufacturing that few Silicon Valley investors are capable of holding. That’s no surprise in a sense: they live and breathe that stuff over there. Furthermore, the government officials have serious budgets and spending capability.

Then there exists a decisive commitment to green energy in China. I found the overwhelming motivation for this in a deeply engrained fear of resource scarcity (rooted in the national trauma of the bitter years), more than a “green” motivation. (Basically, when the Saudis find another oil field, American politicians think “great, we’ll be able to buy more oil from there” — while the Chinese officials think “so what, it’s their oil not ours; we still need to figure out how to get our own energy to take care of our people”.) The commitment to green energy is implemented very clearly at every level of governance. For example, at one point, one senior regional party secretary sat down with me and took an hour with me to go through his 5-year plan, underlining every word where he saw I’d be able to help him with on green energy. Underlines everywhere. This was a senior officer who knew very desperately: No green milestones met, no further promotion. And while in a secondary city, he had a $1B budget to do things with.

Another aspect is of course the presence of a well-oiled, deep, and flexible supply chain. Even as wages increase to Western levels in China, the existence of this will make China continue to be the preferred location for making things.

Meeting with senior gov officials. Agreement on the creation of a 1000-acres “green energy park”. By receiving land from the local government, one can then turn around and obtain a sizable loan from a state bank that is secured against the assessed value of that land. Local government, assessors, and banks work very efficiently with each other and the process is very streamlined. The legal documentation for sizable loans is perhaps 1/100th in size of what it would be in the U.S.

Furthermore, the local government takes responsibility for delivering building and utility infrastructure to one’s spec. At Nanosolar, I once had to pay $10m of our precious equity dollars for basic utility upgrades in our California factory. In our European factory, we managed to cover 50% of such expenses through EU subsidies. In China, one gets that for free, and the government even takes over a lot of the project management.

Left: Our Shanghai area battery factory in a secondary city with approx 7 million residents. Workers’ dormitory included. Fish pond too.

Right: On the morning of meeting with one of China’s top-top officials in Beijing. The entire leadership from our factory’s city went on a 14-hr train ride in support of this meeting in the capital. No display of fireworks on that occasion — but a neat convoy of 16 government limousines — all high-end Audis — with those very special license plates that make any Chinese gasp in awe and call home. (A by-stander did.)

Meeting with a regional Party Secretary near Inner Mongolia. Surveying a 30-sqm site for building a large solar power plant.

Government officials are very decisive in China. At one point during our survey, I noticed some people living in huts on the acreage they showed us. That led to some shouting in Chinese in a meeting the same day after which a translator confronted me, saying “If you desire, the Secretary will now give orders to resettle the people you saw. It’s your call.” Well, after further inquiry, I figured out that these are 40,000 people in a village and given the early stage of the project, I looked for a graceful way not to be responsible for evicting 40,000 people. But I have no doubt that they were serious about doing so.

The government nexus has its challenging aspects too in China. Unlike in Silicon Valley, state supported investments tend to require a “real downside” on the part of the entrepreneur in the event of failure (beyond anything practiced or legal in the United States). Perhaps because failure is not an option, one can find relatively many businesses in zombie existence as well. Then while legal documentation is refreshingly light in China, the flip side of that is a constant dialogue necessary with the government to make sure one is still within the spirit of the understanding. It takes a highly skilled FTE to do that.

Not being a politician, my world view is based on a model of global collaborative value-add more than national boundaries. I see China as a ready customer for innovation produced elsewhere and enabling the roll-out of that innovation at scale. Chinese are highly receptive to foreign innovation and ready to help bring it to scale. The analogy is that without Cisco or Google, startup innovation in these respective industries would be much less investible and look much thinner. In greentech, there’s no Cisco or Google which can provide some level of fail-soft for innovation. But there’s China.

Given the geographic distance and the disparities of culture and language, it is certainly easy for misconceptions to get in between the collaborative opportunities that exist, and they do to a larger extent than necessary. Curiously, a whole number of “idiosyncracies” in China tend to remind me of things I’m familiar with from European culture — the disconnect between American and Chinese culture is probably bigger than that between European and Chinese. For one, the typical Chinese manufacturer is very accustomed to collaboratively working with European tool suppliers, and they have done so for a few decades before Nixon visited China. If the U.S. does not stay relevant to China, China will just strengthen bilateral relationships that already exists very strongly with other countries — something not all that visible in the U.S.

Along the lines of bridging misconceptions, a few words on environmental regulation and intellectual property protection based on my own experience:

While some may view environmental regulation as tough in California, I found it distinctly tougher in China. Past reputation is not necessarily existing practice — my recent direct experience is that oversight is very strict. With a ‘real downside’ for those who make a mistake on that, very unlike in the U.S. The key difference is between following rules and “shit happening”. The former one makes sure about anywhere but the latter can still happen. In our factories in California and Berlin, we never really had to sweat over environmental compliance because the rules are clear and lack of negligence is the standard applied. But in China the ‘real downside’ on accidents happening is very clear and can lead to dramatic pain. Combine this with the fact that Chinese law does not recognize corporations as a purely abstract person but always requires a human legal representative as an anchor for every corporate entity, and you have a different level of consequences.

As for IP, many fault China on that. Many of these same people have not cared to file a single patent ever in China. So first of all, if you want your intellectual property to be worth something in China, you have to file for patent protection over there. That’s true for any place on earth; patent protection only applies in the regions you filed for it. It surely costs a lot to cover the world, and I have made mistakes on that in the past as well. It’s part of what’s broken with the patent system. But that’s unrelated to China. Secondly, my (not-so-joking) joke is that there’s one place on earth that’s worse than China in terms of intellectual property protection — and that’s Silicon Valley. In Silicon Valley, you have engineers leaving a company and an investor right there ready to fund them to create a competing startup right next door. VCs do so routinely. They pick up ideas in board meetings of one company and the next week have funded a company based on that. I’m actually not complaining about that; I’m just saying don’t unfairly single out China. (As far as I’m concerned, the whole patent system is a net negative on innovation, and we would do better without it.) Then also, when violations happen, fixing them is rather effective in China. If you have a government relationship in particular, one can enforce rights very efficiently. If there’s someone stealing your tradesecrets and starting a competitor in the same province, with the right phone call, one can visit the guys in jail the next day. In the U.S., if there’s a violation, it’s the lawyers making money for the next four years and then you settle and have a grown-up competitor.

While I’m back based in San Francisco now, I love the pace and energy in China and continue to be on the board of one China based company and involved in various China activities, in particular also in the Internet space.

Some creations endure centuries. I’ve always had great admiration for things that truly last. Usually, there’s craftmanship involved that builds up over long periods of time.

In my own family history, one of my greatgrandfathers built great furniture:

Door built by my (great)*grandfather in 1772, Bavarian National Museum, Munich.

A hundred years later, this craftsmanship developed to this point:

The King’s bedroom in the “Disney castle”, Neuschwanstein, Germany, built by my greatgrandfather.

Another hundred years later, this line of work went out of business — no-one willing to pay for such work any more was the word. (Then again, just a few decades later, we’ve got Russian oligarchs needing seemingly just that kind of expertise for equipping their yachts.)

AI has always been a top fascination for anyone working with computers; it was certainly mine from my teenage years on and during its first peak in 1991 before the advent of Internet tech then occupied us all.

When Bill Gates donated to the construction of the new computer science building at Stanford, in 1996, giving us all nice offices with windows, he too said during the opening how he was anxious missing out on all the advances in AI about to happen when starting Microsoft. (He also complained back then, in 1996, that for the $6m he donated for the building, he sold MSFT stock that a few months later had appreciated a good percentage. Well, it appreciated 100x until today, making this effectively a $600m donation!). In any case, the fascination with AI is clear and there’s been many approaches and most of them quite fruitless.

When I got the chance of working at Xerox PARC in Palo Alto (along with Reid Hoffman and others) with a Stanford professor as a teenager, I sat in on David Rumelhart’s research group meetings in the psychology department at Stanford during a summer. In hindsight still, they were the most magical research group meetings I’ve ever attended. It’s the reason I embarked on a PhD at Stanford. David invented the backpropagation algorithm that is now the basis of most all AI. People don’t mention him that much any longer because, for one, he is dead and furthermore his contribution is complete standard now everywhere.

I also worked at Siemens neural network group in 1991 in Munich, coding a new type of a radial backpropagation system from scratch starting with a C compiler. I ended up presenting it at the best conference in neural network, NIPS, in 1991 as a teenager. Back then Geoff Hinton, etc. were already sitting in the first row at these conferences and everyone was worried about getting a question from him about whether the brain actually works like this. (It is with great relief in 2023 that I now read he no longer cares and in fact the algorithms we have may well be better than the brain’s).

When I joined Stanford then in computer science, the surprise was that there was exactly no interest in neural networks by any faculty. They were all “symbolic systems” guys, with no knowledge of floating point numbers and how to multiply them with each other in matrices. I sort of had to hide my interest in neural network learning. It’s quite stunning how entire communities of intelligent people, awarded jobs at prestigious places, can be entirely wrong. There was surely interest in knowing about the power of data based learning. At Xeroc PARC in 1991, I witnessed how computational linguists went through some hours each week trying to learn about conditional probabilities in statistics. It was a hopeless effort of course. Their backgrounds were too different. I also so how some of the top leaders in research at PARC took the gutsy approach of saying to today’s now dominant form of artificial intelligence that “If that’s the solution, then I wasn’t interested in the problem.” I was shocked back then about such blissfulness as I am today finding how dead wrong that was.

I just saw a Youtube of nVidia CEO Jensen interviewing one of the technical founders of OpenAI, and he recounts on how he smartly picked neural nets over Bayesian networks and other systems as a basis for his big breakthrough now. It’s a bit funny because guess what — that was a necessary but not sufficient accomplishment made by exactly each best graduates in each year for each of the past 30 years, the exact same conclusion yet landed in history in the wrong year!

Undeniably this year is different now as of 2023, finally! What’s different? Well, Google put up a lot of R&D funding and developed a critical mass of chip and research power; and nVidia nailed it with GPUs.

And recalling Rumelhart, it is equally stunning that a psychology professor figured it all out! Backpropagation is possibly as good as it gets in learning because it assigns blame for errors in the exact fraction of the contribution made to the error. What could possibly work better. The human brain does not use it — but at its peril!

I am excited that after decades (!) I am back now supporting this area with faster chips!

Time wise, since our inception, Nanosolar had usually tracked 2-3 quarters behind our competitor Miasole, including later in production volume ramp. Some journalists criticized Nanosolar for that, not always with a fair understanding. While the product is essentially the same, the inside of the product is distinctly not. From the beginning, Nanosolar was shooting for far more aggressive inside targets: three times better semiconductor materials utilization than Miasole; one third the cost of their cell foil; a factor higher tooling productivity; etc. Benefits of such magnitude don’t just come out of nowhere for free. When Miasole “just” developed new tooling design, Nanosolar had to that plus develop completely new materials processes. When Miasole could rely on a known process, Nanosolar had to invent a completely new one. This put Nanosolar by design on a very different timeframe. All investors knew about it and had bought into it. Given expectations of a commoditizing industry, investing into a company that would achieve a more fundamental cost advantage is a good idea even if it takes longer to get there. Still it’s difficult to communicate this at times, and it became somewhat of an obsession of the press to track this. And it’s virtually impossible to accelerate on a moment’s notice when a board member sees a competitor filing to go public and suddenly feels we ought to as well.

Time wise, since our inception, Nanosolar had usually tracked 2-3 quarters behind our competitor Miasole, including later in production volume ramp. Some journalists criticized Nanosolar for that, not always with a fair understanding. While the product is essentially the same, the inside of the product is distinctly not. From the beginning, Nanosolar was shooting for far more aggressive inside targets: three times better semiconductor materials utilization than Miasole; one third the cost of their cell foil; a factor higher tooling productivity; etc. Benefits of such magnitude don’t just come out of nowhere for free. When Miasole “just” developed new tooling design, Nanosolar had to that plus develop completely new materials processes. When Miasole could rely on a known process, Nanosolar had to invent a completely new one. This put Nanosolar by design on a very different timeframe. All investors knew about it and had bought into it. Given expectations of a commoditizing industry, investing into a company that would achieve a more fundamental cost advantage is a good idea even if it takes longer to get there. Still it’s difficult to communicate this at times, and it became somewhat of an obsession of the press to track this. And it’s virtually impossible to accelerate on a moment’s notice when a board member sees a competitor filing to go public and suddenly feels we ought to as well. As Nanosolar grew into a business with a heavy international and operational activities, one key mistake I made was to not sufficiently evolve the company’s board of directors. The individuals from the early-stage venture firms tend to be people with a good skill set at scouting out promising Bay-area startups. But as a company grows and the executive team matures through senior additions (and as the venture investors percentage of contributed capital shrinks to a small fraction — just 5% in our case), it is important to have a board of directors with deeper business operating, management, international, and industry experience. A real operating business and the world at large out there is just very different an animal than what a typical venture investor tends to get exposed to within the Silicon Valley horizon. By not ever really being in front of customers and suppliers and in touch with the industry at large, it’s actually quite difficult for a venture investor to scale with the company and maintain a good instinct about what’s going on. (I have actually found hedge-fund investors to be very much more in tune with the industry — that’s because they tend to know/visit/track the key other companies, etc.) Then board meetings tend to be a subtle thing and if someone has his instinct in odd places, it makes things difficult. The issue is simply also that during inevitably arising operating challenges, when steadiness is often the best prescription, a VC director with no operating experience tends to get weak in his knees overly quickly and often causes more damage than good. Then it is good to have other board members around to balance the group and point the board discussion onto what matters most. Unfortunately, a lot of damage can be caused by not having an effective board of directors.

As Nanosolar grew into a business with a heavy international and operational activities, one key mistake I made was to not sufficiently evolve the company’s board of directors. The individuals from the early-stage venture firms tend to be people with a good skill set at scouting out promising Bay-area startups. But as a company grows and the executive team matures through senior additions (and as the venture investors percentage of contributed capital shrinks to a small fraction — just 5% in our case), it is important to have a board of directors with deeper business operating, management, international, and industry experience. A real operating business and the world at large out there is just very different an animal than what a typical venture investor tends to get exposed to within the Silicon Valley horizon. By not ever really being in front of customers and suppliers and in touch with the industry at large, it’s actually quite difficult for a venture investor to scale with the company and maintain a good instinct about what’s going on. (I have actually found hedge-fund investors to be very much more in tune with the industry — that’s because they tend to know/visit/track the key other companies, etc.) Then board meetings tend to be a subtle thing and if someone has his instinct in odd places, it makes things difficult. The issue is simply also that during inevitably arising operating challenges, when steadiness is often the best prescription, a VC director with no operating experience tends to get weak in his knees overly quickly and often causes more damage than good. Then it is good to have other board members around to balance the group and point the board discussion onto what matters most. Unfortunately, a lot of damage can be caused by not having an effective board of directors.

Left: Our Shanghai area battery factory in a secondary city with approx 7 million residents. Workers’ dormitory included. Fish pond too.

Left: Our Shanghai area battery factory in a secondary city with approx 7 million residents. Workers’ dormitory included. Fish pond too.